Bank Update: Some Top 10s, Some Not Top 10s, & Hidden Value to Be Uncovered

Short & sweet today.

The quarter is ending (wow this year flew) and it’s time to re-evaluate the bank landscape using some common sense, a little bit of analytical thinking, and a vibe check.

I put together these screens to orient to the world and figure out who I want to track going into earnings season. They key for me is figuring out where the consensus is wrong, where someone is cheaper than they should be, where someone is more expensive than they should be, and where people aren’t paying attention when they should be.

And (insert shameless plug here) if you want to discuss individual names and get more daily thoughts including some posts on valuations, earnings, & longs then join the chat here. We’re building a community of bank & financials friends trying to outperform.

Broadly speaking, it should be a boring quarter for bank earnings and people will be focused on “the guide”. KRX is expected to do 15% EPS growth in 2025 and credit for now is still benign. C&I and Consumer has been stressed because of high rates, but that trend is changing. And CRE has been in the “doom loop” news cycle since NYCB puked up their rent regulated MF provisions, but otherwise it’s been all quiet on the western front. Seeing some chatter on some OZK deals that should be topics of discussion in Q3 earnings as well.

If you invest in banks, the way to win from here going forward is to find banks at the extremes or edges where expectations are not in line with future reality. Or said another way, pick up on narratives before they happen. Soros talked a lot about it in "The Alchemy of Finance” about him and Drucknmiller’s time together. It’s a dense but fantastic read. The main point being this, the way to make money is to see some type of a trend before other people notices it’s there and to bet on it. Simple. At least in theory. I also love the book because it points out that markets cannot be rational since they’re made up of irrational participants. And trust me, we’re all irrational.

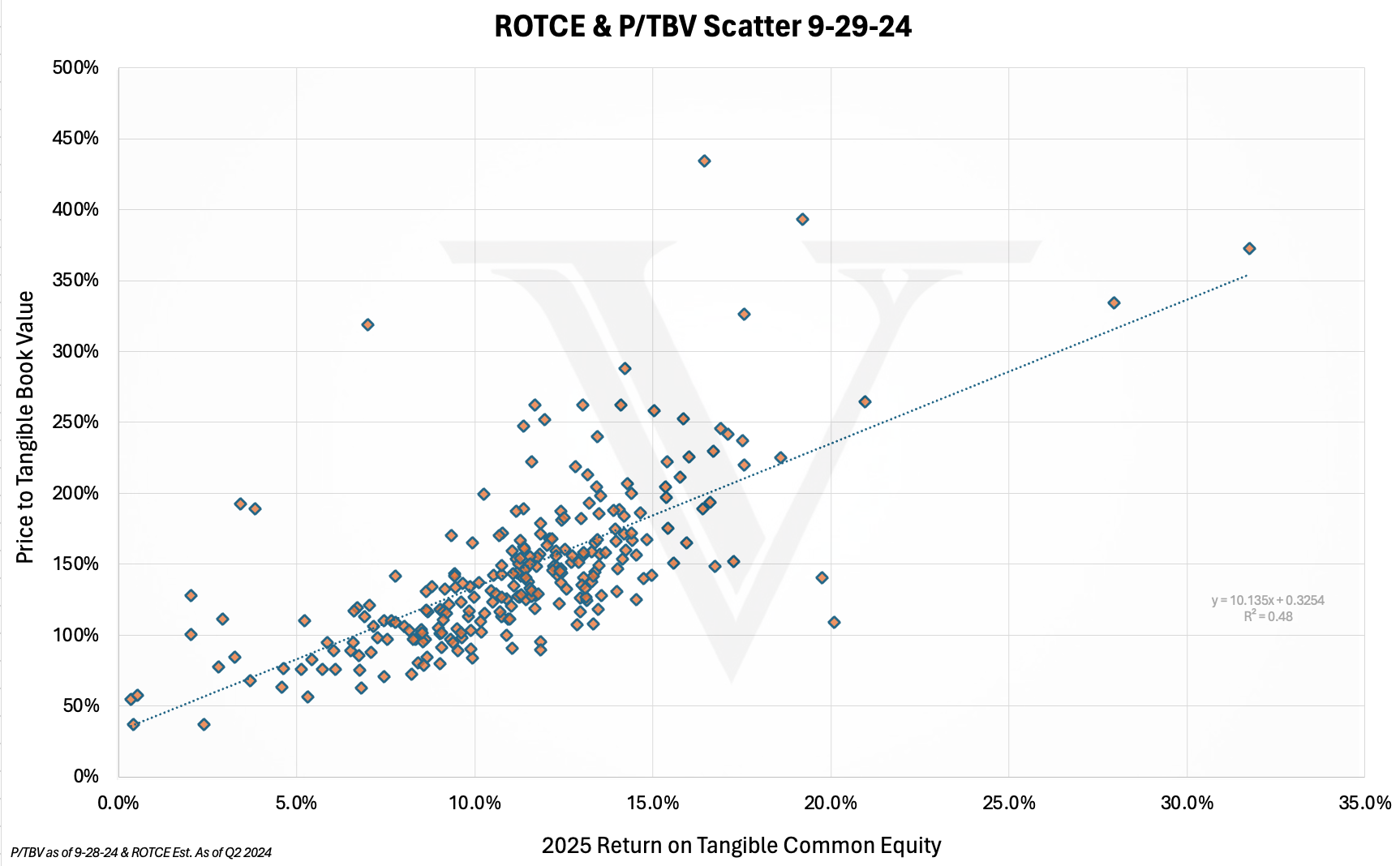

What’s a ROTCE Worth Anyways?

In banks, ROTCE (Return on Tangible Common Equity) and P/TBV (Price to Tangible Book Value) are closely linked because they both reflect how well a bank is performing & priced. ROTCE measures how effectively a bank uses its tangible equity to generate profits. When a bank is good at making money (high ROTCE), it signals strong profitability and efficiency. This, in turn, makes investors value the bank more highly, which raises the P/TBV ratio. Essentially, if a bank is performing well and generating strong returns, investors are willing to pay more for its tangible assets, creating a direct correlation between ROTCE and P/TBV. Tangible book value is a measure of value created for shareholders and price then is a reflection of whether or not investors think you’ll create more value or less value than implied in the future.

Higher than trend = people love you

Lower than trend = people question you

To start, here is the current “What is a given forward ROTCE worth?” graph for all banks with 2025 estimates which is about 254 banks (plus or minus a couple takeout candidates waiting for deals to close).

A 2025 15% ROTCE is “worth” around 170% of TBV.

Whereas a 10% is “worth” around 140% of TBV.

And if you’re CASH, a 32% forward ROTCE is “worth” about 370% of TBV.

Wu Tang Clan said, “cash rules everything around me”. For banks, ROTCE rules everything around you.

The following analysis is going to be for all banks with forward estimates FYI, which is about 250 or 260.

All Banks ROTCE & P/TBV:

But before we move on, I want to highlight one big trend going on. Mainly that larger banks are carrying higher valuations given the same ROTCE. To hit this home, take a look below. This is the same screen, but with only small caps and lower (under $2 billion market cap). Below, you can see that smaller cap banks that produce a 10% ROTCE are only worth 130% of TBV.

Keep reading with a 7-day free trial

Subscribe to Victaurs to keep reading this post and get 7 days of free access to the full post archives.